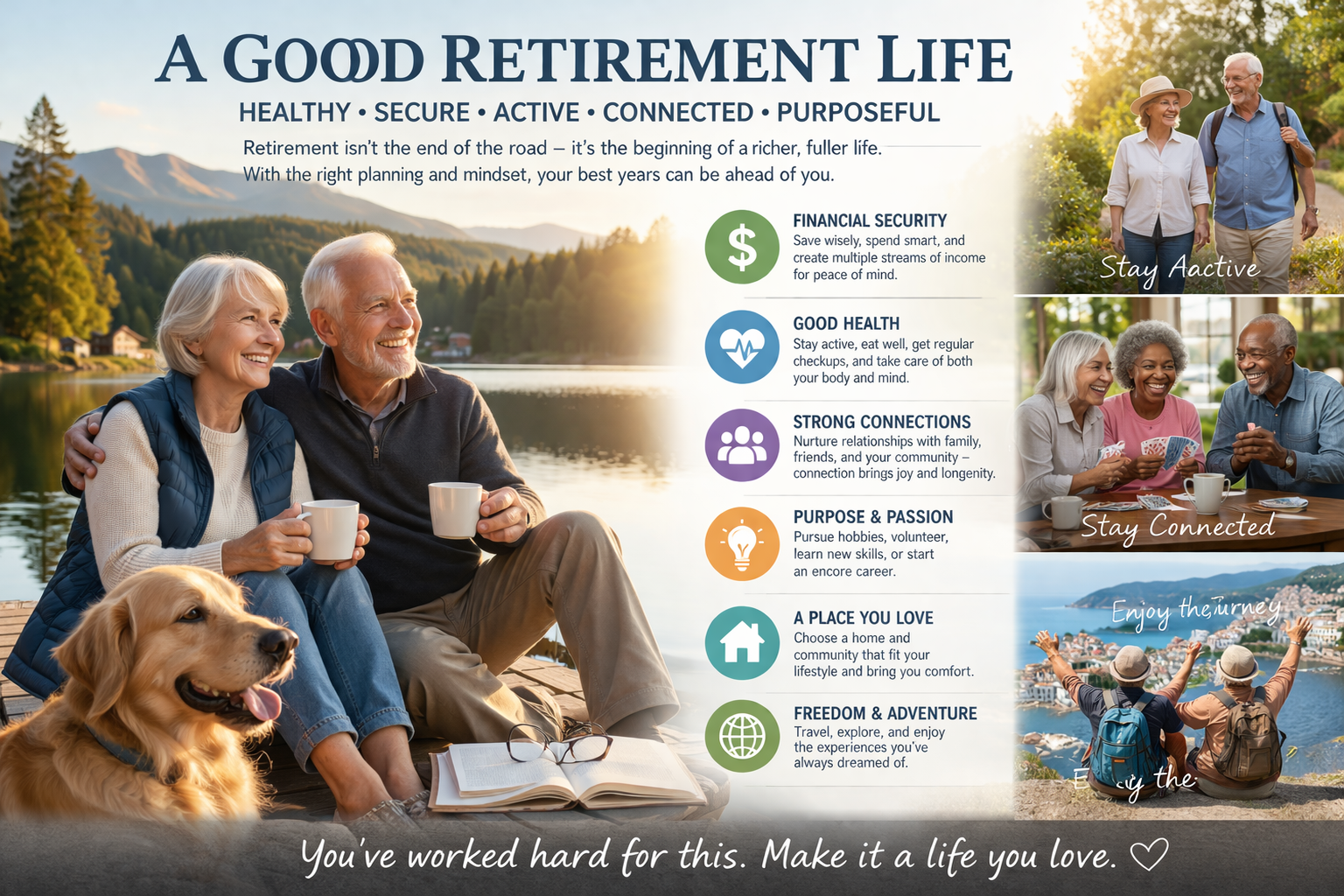

A Blueprint for a Fulfilling Retirement: Planning, Living, and Thriving

Retirement is no longer just an endpoint—it’s a major life phase that can span 20–30 years or more. Thanks to longer life expectancy, evolving financial tools, and shifting cultural attitudes, retirement today offers both opportunities and challenges. Achieving a “good” retirement requires thoughtful planning across finances, health, lifestyle, and purpose.

The New Reality of Retirement

In the past, retirement often meant a short period of rest after decades of work. Today, with life expectancy in the U.S. averaging around 77–80 years—and many people living well into their 80s or 90s—retirement can last as long as a full career.

Programs like Social Security Administration and retirement accounts such as 401(k)s and IRAs have replaced traditional pensions for many workers. This shift means individuals now bear more responsibility for funding their retirement.

Financial Foundations: The Cornerstone of Retirement

A secure retirement starts with solid financial planning.

How Much Do You Need?

A common guideline is the “80% rule”—aiming to replace about 70–80% of your pre-retirement income annually. However, this varies depending on lifestyle, healthcare needs, and debt.

Financial planners often reference the “4% rule,” based on research by William Bengen, suggesting retirees can withdraw 4% of their savings annually with a reasonable chance of not outliving their money over 30 years.

Key Income Sources

- Social Security: Provides a baseline income; benefits depend on earnings history and retirement age.

- Employer-sponsored plans: 401(k), 403(b), and pensions (if available).

- Personal savings and investments: IRAs, brokerage accounts, and real estate.

- Annuities: Offer guaranteed income streams but vary widely in cost and structure.

Rising Costs

- Healthcare is one of the biggest expenses. A 65-year-old couple may need hundreds of thousands of dollars for medical costs in retirement.

- Inflation erodes purchasing power over time—especially critical over a multi-decade retirement.

Health: Your Most Valuable Asset

Financial security means little without good health.

Physical Health

Regular exercise, balanced nutrition, and preventive care are essential. Activities like walking, swimming, and strength training help maintain mobility and independence.

Programs like Medicare provide coverage starting at age 65, but they don’t cover everything—long-term care is a major gap.

Mental and Cognitive Health

Staying mentally active is just as important. Studies show that engaging in learning, puzzles, reading, and social interaction can reduce the risk of cognitive decline.

Purpose and Identity After Work

One of the most overlooked aspects of retirement is the psychological transition.

Work often provides:

- Structure

- Social interaction

- A sense of purpose

Without it, retirees can feel lost or isolated.

Finding Meaning

Many retirees thrive by:

- Volunteering

- Pursuing hobbies

- Starting small businesses

- Mentoring younger generations

The concept of “encore careers”—popularized by thinkers like Marc Freedman—encourages retirees to pursue meaningful work that benefits society.

Social Connections: The Longevity Factor

Strong relationships are one of the biggest predictors of happiness in retirement.

Research, including long-term studies like the Harvard Study of Adult Development, shows that social ties are more important to longevity and well-being than wealth or fame.

Ways to stay connected:

- Join clubs or community groups

- Stay close with family and friends

- Engage in group activities or classes

Where You Live Matters

Housing decisions can significantly impact retirement quality.

Options Include:

- Aging in place: Staying in your current home with modifications

- Downsizing: Reducing costs and maintenance

- Retirement communities: Offering amenities and social opportunities

- Relocating: Moving to areas with lower costs of living or better climate

Some retirees choose states with no income tax or lower property taxes to stretch their savings further.

Managing Risks in Retirement

A good retirement plan accounts for potential risks:

- Longevity risk: Outliving your savings

- Market volatility: Investment downturns

- Healthcare costs: Unexpected medical expenses

- Inflation: Rising costs over time

Diversification, conservative withdrawal strategies, and emergency funds can help mitigate these risks.

The Role of Timing

When you retire affects your financial outlook.

- Claiming Social Security early (age 62) reduces monthly benefits.

- Delaying benefits until age 70 can significantly increase monthly income.

- Continuing to work longer allows for more savings and fewer years drawing down assets.

Technology and Modern Retirement

Technology is reshaping retirement:

- Telehealth improves access to care

- Online banking simplifies financial management

- Social media and video calls help maintain relationships

- Remote work enables part-time income opportunities

Happiness in Retirement: What the Data Says

Research consistently shows that retirees who are happiest tend to:

- Have a clear sense of purpose

- Maintain strong social connections

- Stay physically and mentally active

- Feel financially secure (not necessarily wealthy)

Interestingly, happiness often follows a U-shaped curve—dipping during the transition into retirement, then rising as individuals adjust to their new lifestyle.

Final Thoughts

A good retirement isn’t just about having enough money—it’s about building a life that is sustainable, meaningful, and enjoyable. By planning ahead, staying engaged, and adapting to change, retirement can become one of the most rewarding chapters of life.

The key takeaway: retirement is not an ending—it’s a transition into a new kind of freedom.